Global populations are ageing at an unprecedented rate, accelerating the rise of the Longevity Economy, which is a demographic segment with growing time, purchasing power, and influence. However, despite rapid technological advancement, many digital systems continue to be designed primarily for younger users, overlooking the lived realities of older adults. In practice, the barrier is not just access, but usability, confidence, and trust. Therefore, making the everyday experience of trying to use essential services reliably in a rapidly digitising world harder. This white paper presents findings from AgeTech Leadership Labs’ (ALL) pilot internship program, in which young researchers engaged directly with older adults in India to understand how Gen E (50+) experiences digital tools and services. The initiative was designed as a listening-led effort to surface friction points in onboarding, navigation, updates, and perceptions of safety, particularly across high-frequency domains such as communication, commerce, and digital payments. This report is part of ALL’s roadmap to build the Longevity Readiness Index (LRI): A modular benchmark of how ready systems are for the Longevity Economy. LRI measures three layers of readiness: Digital experience, physical/service infrastructure, and economic readiness and cost pressures. Within “digital experience”, ALL is developing the Digital Usability Score (DUS) as an initial LRI module focused on the digital layer: A practical metric designed to capture how easily Gen E can use a digital app or service over time with minimal confusion, anxiety, or external help. Importantly, DUS is not a measure of a user’s capability but rather a measure of usability, where “usability” refers to the cognitive, procedural, and trust-related ease a user experiences when encountering errors or changes in everyday tasks (e.g., paying, ordering, booking, messaging). Through surveys and in-depth interviews, the pilot identified a consistent pattern: Older adults recognise the value of digital technologies and are willing to adopt them when benefits are tangible, but many experience repeated breakdowns at specific points. Participants described difficulty with sudden app updates, shifting interface layouts, frequent pop-ups, unclear verification cues, and uncertainty around what is safe or reversible. These frictions discourage deeper feature use, increase reliance on family support, and contribute to sustained digital exclusion even among connected users. Rather than presenting definitive conclusions, this paper offers thematic insights intended to inform product design, service delivery, and policy conversations. It also recommends the next phase of work: Translating these insights into a practical DUS scoring approach and validating it through expanded user studies and structured input from industry experts. Over time, ALL will extend the LRI framework beyond digital usability to include complementary readiness measures for physical services and infrastructure, as well as economic indices that shape longevity-era affordability and participation. Download the White Paper here: Designing The Digital Usability Score for Gen E

The Architect of the Second Innings: Why JA Chowdary Is a Longevity Economy Superstar

In the Longevity Economy, we track three metrics: LifeSpan (how long we live), HealthSpan (how long we stay healthy) and WealthSpan (how long we are financially secure). But at AgeTech Leadership Labs, we believe the most critical metric is still missing: PurposeSpan. PurposeSpan is the ability to stay driven, relevant, and contribute well beyond traditional working years. It is the refusal to let a retirement date define your usefulness to the world. This week Longevity Superstar JA Chowdary is the living definition of PurposeSpan. Most people know JA Sir as he is found all called for his role in India’s technology story. Working alongside Chandrababu Naidu, he helped translate vision into execution, playing a pivotal role in building HITEC City and transforming Hyderabad into a global tech hub. He helped create the infrastructure that allowed India to compete with the world. That achievement alone would have been enough for a legacy. Most people would have stopped there, played golf, joined a few boards, and looked back. The Second Innings: Building People But high-purpose individuals don’t stop. They pivot. JA realized something uncomfortable: while the cyber towers rose, the benefits hadn’t reached the villages. Technology disruption was accelerating, and without intervention, the next generation of rural talent risked being excluded—not because of lack of ability, but lack of access. So he shifted his focus from concrete to consciousness. Through his two initiatives – International Startup Foundation and JuniorCorns, JA is now doing for rural children what he once did for multinational companies giving them a platform to scale. He isn’t training them to be employees in a shrinking job market. He is preparing them to become employers. The Longevity Effect I’ve seen the impact up close. More than 150 JuniorCorns, children from tier-2 and tier-3 towns, some as young as 11 are now pitching ideas, travelling globally, and working on real-world problems. Some had never seen an airport and thanks to his efforts have traveled to Dallas last year and to Dubai this year – he literally gave them wings to fly!. Now, these kids are beginning to see themselves as future CEOs. That shift in self-belief is the real outcome. The Insight JA Chowdary shows us that the Longevity Economy is not about “old people.” It is about inter-generational transfer—taking the wisdom, networks, and credibility earned in the first 50 years and reinvesting them into the next generation. He isn’t spending his social capital – He’s compounding it. Meeting JA Sir comes with a warning: his PurposeSpan is contagious. You can’t be around him without confronting an uncomfortable but necessary question: Years are being added to your life. But what are you adding to your years?

Sunday Longevity Superstar: Warren Buffett — The Man Who Quietly Lived the 100-Year Life

Last week, for Trending Tuesday, we looked at the book The 100-Year Life by Lynda Gratton and Andrew Scott, which reshaped global thinking about what it means to live, work, and thrive across a century-long lifespan. Their central argument was profound yet straightforward: in an age when people routinely live to 90 or 100, the future, as we at AgeTech Leadership Labs define it, will belong to those who can align four essential spans: LifeSpan, HealthSpan, WealthSpan, and PurposeSpan. This alignment isn’t merely a personal aspiration; it is the foundation of the Longevity Economy. It determines whether long life becomes a crisis or a form of compounded opportunity. The truth is, very few people manage this alignment. Most excel at one or two spans and struggle with the rest. Some build wealth but sacrifice health. Some discover purpose but lose financial resilience. Many live long lives but without meaning or vitality. Yet every once in a while, a single human being becomes a living case study — not because they pursued longevity, but because the way they lived naturally aligned the four spans over time. This week, as Warren Buffett steps down from the CEO role at Berkshire Hathaway at the age of 95, we honour him not only as the Oracle of Omaha but as one of the rare individuals who quietly lived the 100-Year Life design long before the concept even had a name. He is ALL Longevity Economy Superstar. The Unlikely Longevity Blueprint If longevity were a science experiment, Warren Buffett’s lifestyle would be the control-group failure. The man eats ice cream for breakfast, drinks five cans of Coca-Cola a day, avoids vegetables except mashed potatoes, and orders the same McDonald’s meals with near-religious consistency. He even joked, “I eat like a six-year-old,” and he wasn’t exaggerating. Yet here he is — 95 years old, mentally sharp, emotionally grounded, and stepping back not because of decline, but because he feels it is time for a younger leadership team to carry the legacy forward. How does a man who breaks every rule of modern nutrition become a case study in longevity? The answer, contrary to popular belief, lies not in his diet but in the deeper alignment of his life. Buffett lived with a level of simplicity, emotional stability, and internal clarity that modern researchers now recognise as strong predictors of healthy ageing. He slept eight hours a night. He avoided stress and drama. He nurtured lifelong friendships, especially with Charlie Munger. He read voraciously, stayed curious, and kept his mind in constant motion. His days were calm, not chaotic — a rhythm of reading, thinking, deciding, and teaching. His happiness came not from consumption but contentment. As he famously said, “The key to happiness is having what you want and wanting what you have.” Genetics may have given him resilience, but it was his aligned way of living that sustained it. When Wealthspan Becomes Contribution Span Wealth is the most visible part of Buffett’s story, but it is not the most important. What matters to the Longevity Economy is how he thought about wealth over decades — as a tool for stability, clarity, and contribution. Early in his life, Buffett discovered the transformative force of compounding. He didn’t just understand it mathematically; he understood it philosophically. “Someone is sitting in the shade today because someone planted a tree a long time ago.” This wasn’t financial advice. It was a worldview. Buffett built Berkshire Hathaway into a powerhouse by avoiding what destroys compounding — leverage, ego, haste, noise. His philosophy of “never risk what you have and need for what you don’t have and don’t need” became a financial version of longevity thinking: preserve your ability to stay in the game. Even in his most recent shareholder letter, he reminded investors: “The great majority of your money remains in equities… Our preference for productive assets will not change.”This is long-term Wealthspan thinking — designing financial life so it survives 50 or 60 years with dignity and security. What makes Buffett exceptional is that he didn’t stop at personal Wealthspan. He evolved it into a Contribution Span. Through the Giving Pledge and over $60 billion in donations, he turned his long-term compounding into long-term impact — supporting vaccines, education, and poverty alleviation around the world. Purposespan: The Engine That Keeps You Young If wealth gave Buffett stability, purpose gave him vitality. The man genuinely loved his work. He didn’t perform the role of investor; he lived it. His days were filled with reading, thinking, and making rational decisions — activities that strengthened the brain rather than drained it. He often described it: “I get to tap-dance to work every day.” Purpose wasn’t a separate compartment of his life. It was the core operating system. Even as one of the wealthiest men alive, he didn’t drift into boredom or excess. He stayed grounded through routine, meaning, and love for the game. His partnership with Charlie Munger was a four-decade masterclass in shared purpose — two men thinking, debating, learning, and teaching together. He also shared a more profound truth: “You don’t get rich by what you earn; you get rich by what you avoid.” Avoiding envy, avoiding noise, avoiding clutter — avoiding the emotional and cognitive toxins that age us from the inside out. His purpose kept him relevant. Purpose kept him mentally young. Purpose kept him compounding through every decade of his life. The Lightness of Living There is a hidden philosophy running through Warren Buffett’s life — a philosophy of lightness. While many accumulate more as they age — more houses, more possessions, more status symbols — Buffett aged through liberation. He lived in the same house he bought in 1958. He drove himself. He kept a small team. He maintained a simple daily structure. He once said, “The best investment you can make is in yourself.” Notice that he didn’t say in things. This is a crucial longevity lesson: – Heavy lives age faster. – Lighter

Markers Monday: Grip Strength, The Handshake Between Health and Longevity

Last week at MarkersMonday, we introduced Grip Strength as a vital marker from the HealthSpan domain, a simple yet powerful predictor of how well we age. This week, we go deeper into the science, economics, and intelligence behind this humble yet revealing measure, and explore how it connects to the broader Longevity Economy through the MTS Framework (Markers, Trackers, Stackers) developed by AgeTech Leadership Labs When longevity becomes the new normal, measurement becomes the new medicine. Among all health metrics, Grip Strength stands out as one of the most robust predictors of biological age, independence, and survival. Scientific Foundations: Grip Strength as a Biomarker Grip strength is measured with a hand dynamometer, which captures the maximum force of the hand muscles in kilograms or pounds. It reflects not only muscular power, but also neurological integrity, cardiovascular efficiency, and metabolic health a whole-body indicator rather than a localized test. Research since the 1980s has consistently validated grip strength as a clinical biomarker of ageing and mortality: A 2018 meta-analysis in The Lancet (Leong et al.) of 140,000 participants across 17 countries found that every 5-kg drop in grip strength correlated with a 16–20% higher risk of premature death, independent of smoking, blood pressure, and BMI. Additional studies have linked lower grip strength to higher risk of heart disease, cognitive decline, mobility limitations, and hospitalizations sometimes with greater predictive accuracy than cholesterol or blood pressure. Grip strength typically peaks at ages 35–40 and then declines gradually, with an annual reduction of 1–2% after 60, influenced by diet, physical activity, and chronic disease. Real-World Applications and Economic Impact At a population level, grip strength is emerging as a macroeconomic variable—a marker that connects physical capacity with national productivity. Japan integrates grip testing in elder care to track functional ageing and reduce long-term dependency. European insurers (Germany, Netherlands) use grip data to design incentive-based wellness premiums. In Singapore, modeling by geriatric economists suggests that a 10% improvement in average grip strength among adults aged 60+ could cut national healthcare costs by 1.2% of GDP annually, through reduced hospitalization and delayed frailty. In the U.S., frailty-related healthcare costs exceed $50 billion per year, with grip strength now widely recognized as a top predictive variable for functional decline. Grip strength, in short, has evolved from a gym test into an economic indicator, one that quantifies the strength of nations as much as individuals. The evidence is clear: grip strength is no longer just a physical measure it’s a health system signal. The MTS Framework: Turning Markers into Meaning To manage what we measure, we must connect what we collect. That’s the mission of the #MTS Framework — Markers, Trackers, Stackers, developed by AgeTech Leadership Labs as the intelligence infrastructure for the Longevity Economy. MTS transforms scattered data from medical systems, fitness devices, and financial trackers into an integrated operating system that links health, wealth, and purpose. Here’s how Grip Strength fits into the model: Marker – Defining What to Measure Grip strength serves as the Marker, with normative healthy ranges of 35–60 kg for men and 20–40 kg for women, adjusted by age and ethnicity. The insight lies in the trajectory—is your grip getting weaker, holding steady, or improving with interventions? Tracker – Measuring the Reality The Tracker captures data over time. Traditional dynamo meters provide snapshot readings, while new wearable sensors and smart grips record micro-changes in strength during daily activity. Linking this data with lifestyle metrics—sleep, nutrition, stress, and exercise—turns static readings into living feedback loops. Stacker – Connecting the Ripple Effects The Stacker layer reveals how one marker influences others across the four spans of longevity: Lifespan: Low grip strength correlates with all-cause mortality. Healthspan: Decline precedes frailty, mobility loss, and metabolic inefficiency. Wealthspan: Weaker grip predicts early workforce exit, higher care costs, and dependency. Purposespan: Physical capability supports confidence, caregiving, and social engagement. Grip strength, in this model, is the keystone marker—strengthen it, and you fortify the system that sustains life, livelihood, and meaning. From Data to Design: Personalized Longevity Networks In an MTS-enabled ecosystem, users could click on “Grip Strength” and instantly view: Their personal trend line How it compares to age-based benchmarks Services, trainers, or digital tools to improve it Ripple effects on other spans (e.g., improved mobility → higher work participation → greater wellbeing) Artificial intelligence then learns from these interactions modeling how changes in one marker influence others. This creates a dynamic longevity network, where data doesn’t just inform but adapts and guides. This is the next frontier: from health tracking to health orchestration a shift from reactive medicine to proactive lifespan design. Conclusion: Grip Strength as a Keystone of Longevity Intelligence Grip Strength transcends its physical dimension. It is a sentinel of systemic ageing, a predictor of independence, and a bridge between biology and economy. When powered by the MTS Framework, it becomes more than a number it becomes a signal for how well individuals, institutions, and nations are preparing for the age of longevity. “What we hold in our hands is more than strength—it is the power to hold our future steady.” Nitin Jaiswal

Mind the Gap: Introducing the Longevity Inflation Index (LII)

This is the follow-up to the Sunday Superstar post, where we explored the concept of inflation-adjusted retirement bonds, inspired by the insightful work of Robert C. Merton and Arun Muralidhar. These innovative bonds aim to hedge retirement income against inflation risk, but a crucial missing link is the inflation index—the benchmark that accurately measures how prices relevant to retirees are rising over time. The Ageing Demography: The global demographic transformation is unfolding at a scale unseen since the Industrial Revolution. By 2050, over one in six people worldwide will be aged 65 or older—up from one in eleven in 2019 (UN World Population Prospects, 2024). Advances in medicine, declining fertility, and improved living conditions have combined to dramatically increase life expectancy. However, this demographic longevity introduces a structural inflation largely invisible to standard economic metrics. While consumer price indices (CPI) and producer price indices (PPI) measure short-term movements in general prices, they fail to capture the compounding costs required to sustain longer lives—costs that include healthcare, long-term care, assistive technology, housing adaptations, and insurance. Why Traditional Inflation Metrics Fall Short for Aging Populations The CPI was designed around the consumption patterns of working-age populations. Unfortunately, retirees experience a dramatically different inflation landscape. Their spending skews heavily toward healthcare and elder-specific services, sectors growing 1.5 to 2.5 times faster than general inflation in many countries (OECD, 2024). For example, healthcare costs have risen 56% between 2010 and 2024, while CPI increased only 28% during the same period (OECD Health Stats). This mismatch causes traditional inflation measures to underestimate the true cost escalation retirees face, leading to serious under-funding in pensions and public programs and risking retirees’ economic security. Introducing the Longevity Inflation Index (LII) AgeTech Leadership Labs (ALL) has researched and designed the Longevity Inflation Index (LII), a new, age-adjusted inflation measure specifically tailored to reflect the spending realities of aging populations. Unlike CPI, the LII adjusts weights toward sectors that dominate retiree spending—healthcare, long-term care, pharmaceuticals, housing adaptations, insurance, and assistive technology—providing a transparent, demographic-driven benchmark. The Economic Imperative for LII Adoption Without incorporating longevity inflation, pension funds miscalculate liabilities by 20-40% over typical retirement spans. This underestimation threatens fiscal sustainability globally and inflates risks for insurers, investors, and individuals alike. The LII offers a practical solution to quantify and address these risks proactively. Global Perspectives: How Longevity Inflation Varies Across Countries Japan: With 30% of the population over 65, healthcare and long-term care costs inflate at more than double the rate of CPI, stressing pension systems (MHLW, 2023). Singapore: Aging 20% population with rising healthcare costs driven by technology adoption and housing expenses. EU: Average 21% elderly population with diverse inflation landscapes but common growth in care-related costs. USA: 17% over 65, regional disparities in healthcare pricing, with experimental CPI-E showing 1.2% higher inflation for seniors. Brazil: 10% elderly share, facing inflation volatility and nascent retirement market reforms. Moving Forward: Collaboration and Next Steps AgeTech Leadership Labs(ALL) which had designed the LII framework and methodology will be publishing a whitepaper LII and inviting interns and other stakeholders for consultation and research partnership. This next-generation inflation metric is critical to future-proofing retirement, insurance products, and social policies to sustain economic security in longevity. Nitin Jaiswal Follow up on this article with our upcoming comprehensive white paper, and join us in shaping the future of aging economies.

Longevity Economy Sunday Superstar : Shinzo Abe

“In a world chasing youth, he designed for age.” While many saw aging as decline, this week AgeTech Leadership Labs Longevity Economy Sunday Superstar Shinzo Abe saw it as destiny — Japan’s path to innovation and resilience. What Makes Abe the Longevity Economy Superstar? As Japan’s longest-serving Prime Minister, Abe understood what many leaders miss: longevity is not just a demographic fact; it’s a design challenge. Under his leadership, Japan became the first nation to treat aging not as a problem, but as a system to reinvent. In 2017, Abe launched the Council for Designing the 100-Year Life Society, inspired partly by The 100-Year Life by Lynda Gratton and Andrew Scott. He posed a simple but transformative question: Japan 100-Year Life Initiative: “If people will live to 100, how must education, work, and welfare systems evolve?” This question laid the foundation for Japan’s 100-Year Life Initiative and Society 5.0— a bold national strategy to build what Abe called a “super-smart society.” One where technology serves humanity, robotics empower eldercare, telemedicine and fintech support independence, and lifelong learning becomes as natural as lifelong work. Abe’s goal was not simply to extend life but to alignlife across lifespan, healthspan, wealthspan, and purposespan. Under his vision, Japan became the world’s first living laboratory for the Longevity Economy. From Okinawa’s celebrated “Blue Zone” communities to progressive employment reforms and the expansion of NISA savings accounts, Abe wove culture, finance, and innovation into a seamless arc of life. He re-framed aging from burden to blueprint, transforming the narrative of decline into one of design. His economic legacy, known as Abenomics, mirrored this longevity logic: balancing stimulus with structural reform, empowering women’s workforce participation, and encouraging early investment to secure financial independence in later years. Focus on WealthSpan and PurposeSpan Abe recognized financial literacy as a longevity skill — the foundation of WealthSpan — and social purpose as a health intervention — the essence of PurposeSpan. His greatest contribution was a paradigm shift: the future belongs not to the youngest or fastest, but to those who prepare for time itself. Though his sudden passing in 2022 froze a moment, his visionary ideas continue to ripple through Japan and inspire the global conversation on “super-aging societies,” “silver entrepreneurship,” and the Longevity Economy. Shinzo Abe didn’t just govern a nation — he mapped the century of life. Longevity Lesson from Abe to the world Leaders At AgeTech Leadership Labs, legacy is measured not by the years we live, but by the systems that outlive us. Abe’s vision lives on in every society learning how to age well, live long, and lead with purpose. Nitin Jaiswal Sunday Superstars of the Longevity Economy is a weekly series that shines a spotlight on individuals whose work and vision are shaping the growth of the Longevity Economy. #SundayLongevitySuperstar #ShinzoAbe #100YearLife #Society5_0 #LongevityEconomy #Healthspan #Wealthspan #Purposespan #Abenomics #AgeTechLeadershipLabs #SilverElephant

Book Insight: The 100-Year Life: Reframing Living, Learning, and Earning in the Longevity Economy

What does it mean to live, learn, and earn across a century-long life? The question sits at the center of a paradigm shift in how societies, businesses, and individuals approach aging. The influential book The 100-Year Life: Living and Working in an Age of Longevity by Lynda Gratton and Andrew J. Scott challenged conventional timelines and introduced a framework that now underpins contemporary policy, business strategy, and personal planning in the Longevity Economy. Since its publication in 2016, Gratton and Scott’s synthesis of human potential and economic evidence has helped millions re-imagine time as a strategic resource, not merely a budget to be stretched. Why this book matters to the Longevity Economy? The authors merge human insight with rigorous economics to argue that longevity is not a burden but a vast opportunity—provided there is deliberate planning, flexible institutions, and bold reinvention. The book’s influence extends beyond academia: it has shaped national conversations, inspiring initiatives that redesign education, welfare, and work to align with longer, more dynamic lifespans. In Japan, for example, gratitude for long life spurred a national blueprint for a 100-Year Life Society, catalyzing policy discussions on how education, employment, and social protection must evolve to keep pace with rising longevity. The idea has also resonated with business leaders and investors who recognize that aging populations are not just a demographic challenge but a market with expanded horizons for products, services, and innovative business models. And while Abe designed for the 100-Year Life, this Sunday’s superstar — Warren Buffett — shows us what it means to live it. Before we meet the sage who embodied that design, here are ten timeless insights from Gratton and Scott’s visionary book — ideas that continue to shape how we live, work, and thrive in the Age of Longevity. Top insights that continue to shape the Longevity Economy The Three-Stage Life Is Over Historically, life followed a straight line: education, work, retirement. Gratton and Scott show how longevity disrupts this trajectory. A century-long life demands ongoing transitions—learning, earning, pausing, and reorienting toward purpose. The future favors those who view life as a series of evolving seasons rather than a single race. What this means today: individuals should plan portfolios of skills, experiences, and networks that can be refreshed repeatedly. Employers benefit from internal mobility—creating internal “career ecosystems” where people shift roles, take sabbaticals, or pursue new disciplines without losing momentum. Policymakers can support this through portable benefits, portable pensions, and access to lifelong learning credits. The New Currency Is Time Money remains essential, but time is the new currency. Longer lives create bigger time budgets but also demand wiser management. Time should be allocated with the same discipline used to deploy financial capital: health investments, ongoing education, and meaningful relationships yield compounding returns over decades. Practical steps: adopt time budgeting alongside financial budgeting; allocate blocks for health maintenance, skill-building, and social connection; design work schedules and retirement ages that reflect personal tempo rather than a one-size-fits-all standard. Reinvention Becomes a Core Skill Identity no longer follows a single, linear arc. People will navigate multiple careers, reinvent interests, and repurpose capabilities across decades. Reinvention becomes a central competence—learning how to retool, rebrand, and re-enter the labor market with confidence rather than hesitation. What to do: cultivate a modular set of transferable skills, maintain a personal learning plan, and embrace portfolio careers. Organizations can support reinvention through modular job designs, continuous training, and safe pathways for mid-life transitions. Health Becomes an Investment, Not an Expense Longer life hinges on a longer HealthSpan. Health is capital—an asset that compounds across time when protected by prevention, sleep, nutrition, and mental balance. In the Longevity Economy, well-being is a core productivity strategy, not a cost center. Actionable habits: prioritize preventive care, genomics-informed wellness where appropriate, and workplace health programs that blend physical, mental, and social well-being. Policy implications include integrating healthspan metrics into employer incentives and public health planning. Purpose Extends Productivity PurposeSpan is the capacity to stay engaged through meaning, not mere obligation. A sense of purpose fuels persistence, creativity, and even longevity itself. People who align work and relationships with deeper meaning tend to sustain vitality longer. Application: organizations should design roles and projects around purpose alignment, and individuals should seek opportunities that provide ongoing meaning—whether through mentoring, community impact, or creative pursuits. Social Capital Is the Hidden Wealth As lifespans lengthen, networks of trust, care, and collaboration become critical. Social capital compounds faster than financial capital and can be the decisive factor in resilience. Longevity without connection is unsustainable. Strategies: invest in diverse, cross-generational networks; cultivate communities of practice; and design social infrastructures that preserve collaboration across life stages. Education Must Last a Lifetime Front-loading education in youth is no longer sufficient. Lifelong learning ecosystems are essential for upskilling, reskilling, and cross-skilling across an extended career horizon. Learning becomes a platform that keeps people relevant in a changing economy. What to build: accessible online and offline learning hubs, employer-supported education credits, and public programs that incentivize continuous skill development across sectors. Financial Resilience Replaces Retirement Security Retirement as a fixed endpoint belongs to an industrial past. Financial systems should adapt to multi-chapter lives, with income, savings, and purpose fluctuating across decades. True wealth in the longevity era means financial agility and resilience, not a single finish line. Implications for individuals: diversify income streams, design flexible retirement plans, and couple savings with flexible spending for health, care, and care-adjacent services. Inequality Is the Longevity Divide Longevity benefits are not shared equally. Access to healthcare, education, and adaptable work determines who truly thrives. Without inclusive policy and innovation, longevity could widen social disparities, creating a future where some live to 100 in comfort while others face precarity. Policy and market responses: universal design for aging in the workplace, equitable access to lifelong education, and targeted social protections for vulnerable populations. Narrative Flexibility Becomes Survival Strength Emotionally and narrative agile living is essential. The 100-year life demands the ability to rewrite personal stories—embracing failure as a learning

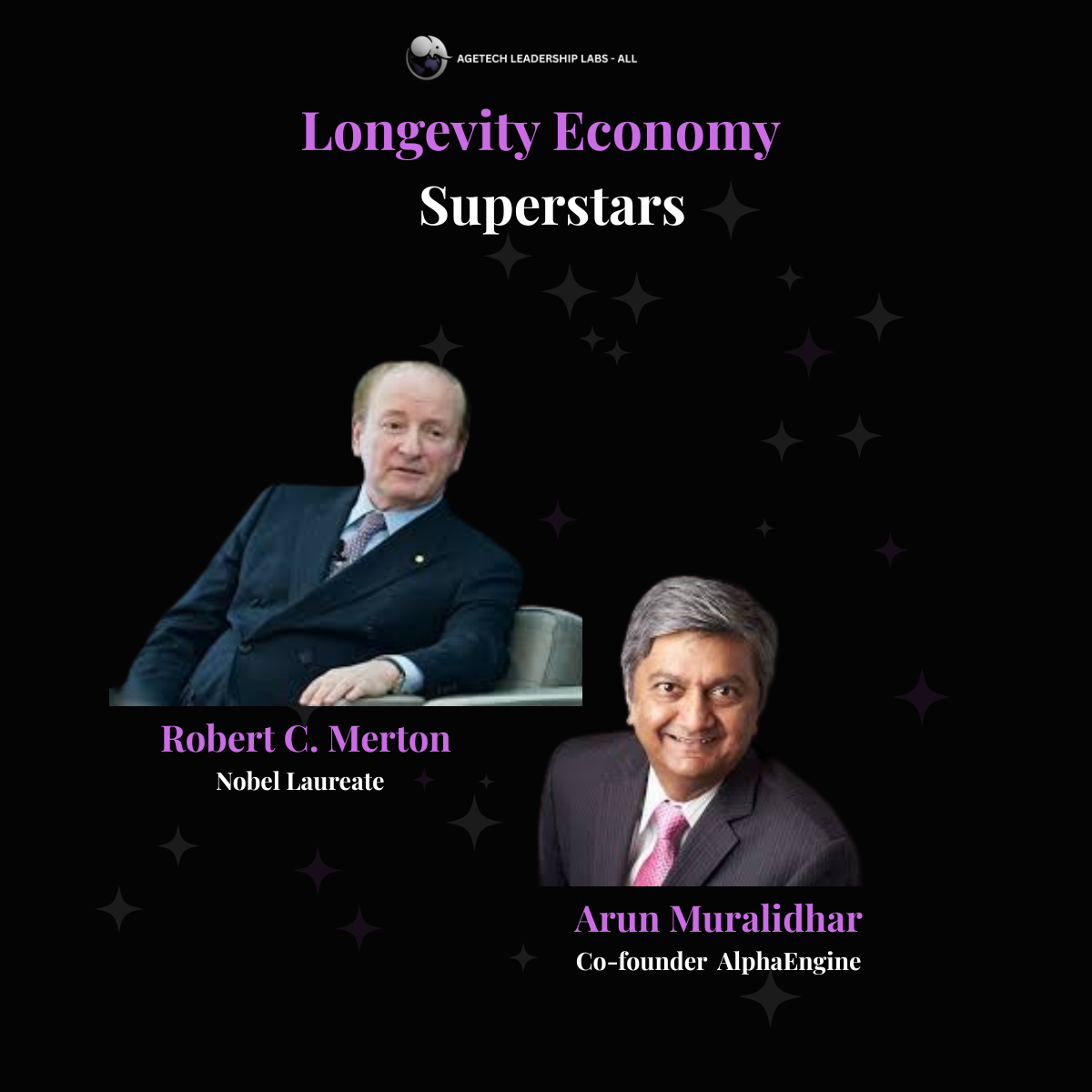

Longevity Economy Superstars: Robert C. Merton & Arun Muralidhar: The Minds Powering the WealthSpan Revolution

For a Healthy and a Wealthy Longevity Economy! Most breakthroughs in longevity focus on how to live longer — new genes, new drugs, new diets. But living longer without financial security is not a gift; it’s a gamble. That’s why this week’s Sunday Superstars of the Longevity Economy, curated by AgeTech Leadership Labs, honor Robert C. Merton and Arun Muralidhar — two brilliant financial thinkers who have re-imagined how the world can sustain wealthspan across longer lifetimes. The Longevity Economy Greatest Problem They Saw Across the world, pension systems are under strain. Lifespans are rising, markets are volatile, and retirement savings often fail to convert into predictable income. Most people don’t know how much to save, where to invest, or how to ensure their money lasts as long as they do. In short — we’ve extended life expectancy, but not financial expectancy. And with that comes another silent challenge: the gradual erosion of purchasing power as people live longer — a kind of longevity inflation that few policymakers are yet measuring, but everyone will soon feel. From Option Pricing to Life Planning Robert C. Merton, Nobel Laureate and MIT Sloan Professor, is best known as the co-creator of the Black–Scholes–Merton model — the mathematical foundation of modern option pricing that reshaped global finance. But in one of the most meaningful pivots of his career, Merton turned his genius from markets to people — applying the same rigor that priced risk to now protect lives across time. Together with Arun Muralidhar, co-founder of AlphaEngine and fellow MIT economist, he set out to solve what Merton called “the nastiest, hardest problem in finance” — how to turn accumulated savings into guaranteed, lifelong income. Their answer: SeLFIES (Standard of Living Indexed, Forward-Starting, Income-Only Securities) also known as Retirement Security Bonds (RSBs). The Longevity Economy Innovation That Redefines Wealthspan SeLFIES are revolutionary because they: Start paying only at retirement — when income is truly needed. Are indexed to living standards or inflation — preserving purchasing power for life. Simplify everything — citizens just decide when they’ll retire and what income they’ll need. The brilliance of SeLFIES lies not in complexity, but in clarity. They shift the global retirement conversation from “How much wealth do I have?” to “How much income security will I have for life?” From Theory to Reality — Brazil’s RendA+ In 2023, Brazil became the first country to bring this concept to life through the RendA+ bond, adapted by Azita Sharif and Alexandre Vitorino in collaboration with Merton and Muralidhar. For the first time, ordinary citizens could buy a simple, government-issued bond that guarantees a lifelong, inflation-protected income stream — a pension fund in a single product. MIT Sloan called it a milestone in financial innovation. In a world where people fear outliving their money, RendA+ gave longevity a safety net. Why They Are Superstars of the Longevity Economy Robert C. Merton and Arun Muralidhar are not merely economists; they are architects of financial dignity. Merton transformed financial theory through the Black–Scholes–Merton model. Together with Muralidhar, he has now transformed financial purpose — ensuring that the benefits of longer life are backed by security, not uncertainty. In doing so, they expanded the very meaning of longevity — from living longer to living securely. Their work bridges finance, policy, and purpose, reminding us that the Longevity Economy is not only about biotech or medicine — it’s also about the systems that make longer lives sustainable. At Nitin Jaiswal at AgeTech Leadership Labs, we salute these pioneers whose innovation inspires us to continue building frameworks that strengthen wealthspan and safeguard the future of financial longevity for all. Because living longer means little unless we can afford to live well. In the end, longevity is not only about lifespan —It’s about livelihood. #LongevityEconomy #WealthSpan #Inflation #LongevityInflationIndex #AgeTechLeadershipLabs #NitinJaiswal #FinancialInnovation #SundaySuperstar

Longevity Economy Superstar Sunday: Piyush Pandey — The Immortal Voice of a Generation

One may be surprised to see Piyush Pandey — the legendary adman of India who dies this week at the young age of 70 years — described as a Longevity Economy Superstar. After all, he didn’t work in biotech, healthcare, or aging innovation. But the Longevity Economy isn’t only about living longer — it’s about living meaningfully and leaving behind an impact that endures. Piyush life is a powerful reminder that the ultimate measure of longevity is not years added to life, but life added to years — and the legacy that continues long after we are gone. As the Chief Creative Officer and Executive Chairman of Ogilvy & Mather India, Pandey transformed the landscape of Indian advertising and, in doing so, helped shape a nation’s cultural memory. From “Mile Sur Mera Tumhara” — the anthem of unity — to “Har Ghar Kuch Kehta Hai” and “Cadbury Kuch Khaas Hai”, his campaigns became emotional touch points for generations. They weren’t just advertisements; they were reflections of who we were and who we aspired to be. Everyone from my generation can trace parts of their childhood to the work of Piyush Pandey — and that is what true impact looks like: when your creations become memories. True Measurement of Longevity – The PurposeSpan Yes, Piyush achieved immense professional success and wealth — but that’s not what people remember. They remember how he made them feel. His storytelling transcended commerce. It touched hearts, built identities, and connected people. That ability to create something that outlives you is what makes him a true Longevity Superstar. In a world obsessed with healthspan, wealthspan, and lifespan, Piyush Pandey reminds us of a fourth and higher dimension — the Purposespan. His purpose, as I understand from reading about him, was not accumulation but creation; not fame, but connection. The legacy he leaves behind teaches a profound truth: we are not remembered for our titles or possessions, but for the emotional imprints we leave behind. Pandey transformed an industry — and, more importantly, inspired generations of creative minds. Nitin Jaiswal at AgeTech Leadership Labs picks Longevity Economy Superstar : Piyush Pandey As we celebrate the launch of Superstar Sunday, honoring individuals who are redefining what it means to build the Longevity Economy, let us begin with Piyush Pandey — not because he lived long, but because he will live on. His work remains our collective inheritance. His legacy, our ongoing inspiration. In the end, longevity is not about time. It’s about timelessness.

Book Insight | Venki Ramakrishnan’s “The Longevity Divide” — Nitin Jaiswal on What It Means for the Longevity Economy

In this Book Insight from AgeTech Leadership Labs, Nitin Jaiswal explores Venki Ramakrishnan’s The Longevity Divide, examining what it reveals about the evolving Longevity Economy — and why, as science bends time, society must ensure it doesn’t break apart. “The dream of ending ageing could easily turn into a nightmare of new inequality ”- Venki Ramakrishnan, Why We Die What if humanity’s greatest scientific triumph – the power to slow or even reverse ageing becomes its most dangerous divide? A new inequality is emerging, measured not in wealth or privilege, but in years of life itself. The Age of the Ageless Scientific advances suggest ageing results from a gradual loss of biological “information.” Harvard geneticist David Sinclair describes this as the body’s equivalent of data corruption – errors that, in theory, can be repaired. His research shows how small, consistent interventions compound over time, multiplying our capacity to live longer, healthier lives. Yet, as Nobel laureate Venki Ramakrishnan asks, who will have access to these breakthroughs if they truly extend life? He warns that if advanced longevity tools remain within reach of only the wealthy, the lifespan and healthspan gaps will grow even wider. The rich already live decades longer than the poor; new technologies could turn that advantage into permanence. This is his idea of Longevity Divide. Time as the Ultimate Commodity Today, billionaires are investing heavily to buy time. Jeff Bezos funds Altos Labs; Google’s Calico dreams of ending death; biohacker Bryan Johnson spends millions a year attempting to reverse his biological age. Meanwhile, one billion people still lack access to basic healthcare. In the United States, men in the top 1 percent of income live nearly 15 years longer than those in the bottom 1 percent; in the U.K., the gap between rich and poor neighbourhoods exceeds eight years. The World Health Organization finds that inequities in income, environment, and access to care shorten lives far more than genetics ever could. Longevity, then, is not just a story of biology, it’s a story of economics and justice. The Next Great Divide : The Longevity Divide Historian Yuval Noah Harari foresaw a “race between castes of mortality.” That race is underway. Technology always diffuses unevenly: a vaccine delayed by ten years costs lives; a longevity therapy delayed by ten years costs lifetimes. The result could be a two-speed humanity, one cohort living beyond 120, another still battling preventable disease before 70. Globally, the gap between LifeSpan and HealthSpan – the years lived in good health has widened to nearly a decade. Science is adding years to life even as inequality subtracts life from those years. The Economics of Extra Years Longevity is macroeconomics with mitochondria. The World Economic Forum values the longevity economy at about $17 trillion annually, reshaping labour, finance, and healthcare. Longer lives could boost productivity and innovation if health gains are broadly shared. If not, time itself becomes a compounding asset. Wealth buys better care, producing more years to accumulate wealth — a feedback loop the WHO calls the social gradient of health. As Ramakrishnan notes, “How long you live may soon depend less on biology than on budget.” Bridging the Gap: The AAA North Star As Nitin Jaiswal notes in his work on the Longevity Economy, inequality grows when access to healthspan innovation is uneven. The question now is not who will live longer but who decides who gets to. Science alone can’t answer that; policy must. At AgeTech Leadership Labs, the guiding principle is the AAA North Star: making longevity Available, Affordable, and Accessible. Available: Breakthroughs must move beyond elite clinics into public health systems, as vaccines once did. Affordable: Markets won’t close cost gaps fast enough; public–private partnerships and open R&D can. Accessible: Tools must work across ages, languages, and digital literacy levels, because exclusion often hides in the interface, not the molecule. The AAA framework links scientific progress to social inclusion, turning discovery into shared opportunity rather than private privilege.The Longevity Divide must be addressed before it becomes a deep valley difficult to navigate. From Vision to Infrastructure Science alone won’t deliver equitable longevity without systems that sustain it. Nations need longevity infrastructure data networks, preventive-care ecosystems, and age-inclusive workforce policies that treat ageing as an opportunity, not a burden. Stanford psychologist Laura Carstensen, author of A Long Bright Future, reminds us that most gains in life expectancy came not from miracle drugs but from sanitation, nutrition, and education. The WHO estimates that closing global health inequities could save millions of lives each year and extend life expectancy in low-income countries by decades. Regulators can accelerate progress by classifying ageing as a treatable condition a step already under debate in the European Parliament. Otherwise, societies may become, in Ramakrishnan’s words, “longer-lived but not better lived.” A Compass for a Longer Century Every technological revolution faces a choice: inclusivity or entrenchment. Longevity science is no different. The AAA North Star offers a pragmatic compass to keep time a public good, not a private asset. If breakthroughs are available across borders, affordable across incomes, and accessible across generations, the gift of longer life can spark a shared renaissance. Otherwise, privilege becomes embedded in biology itself. As economist Andrew J. Scott writes, “More time is our most valuable resource. The question is what we do with it and who gets enough of it to choose.” The 20th century gave humanity universal education, electricity, and vaccines. The 21st must do the same for extra years of life. Progress should not be measured by who lives longest, but by how many live well, longer. At AgeTech Leadership Labs, Nitin Jaiswal continues to shape the Longevity Economy dialogue for a more inclusive future